Amber Galvan

Amber Galvan- +1(561) 914-2664 amber.galvan@lptrealty.com

Facing Pre-Foreclosure? Here’s What You Need to Know

If you’re reading this, chances are you’ve received a Notice of Default or a foreclosure warning from your lender. First, take a deep breath. You are not alone, and this doesn’t mean you’re out of options. Many homeowners in your position feel overwhelmed, unsure of their next steps, and afraid of losing their home—but there are ways to take control of the situation before it’s too late.

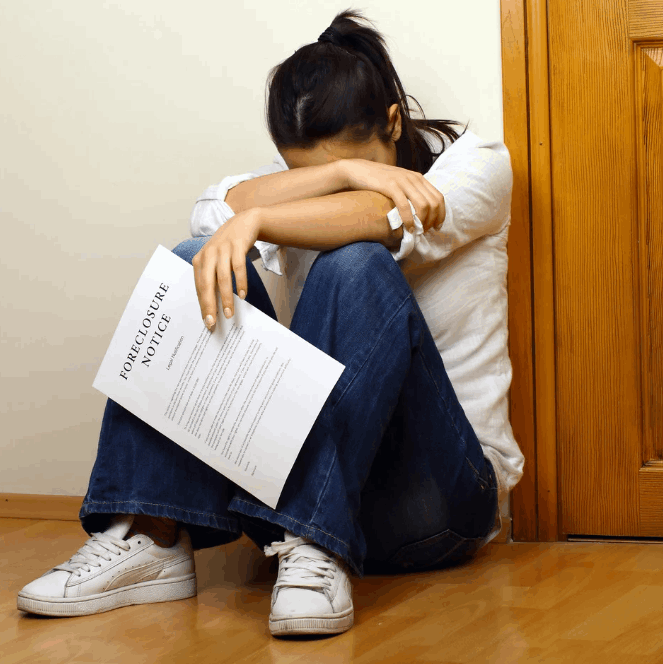

What Is Pre-Foreclosure?

Pre-foreclosure happens when a homeowner falls behind on mortgage payments, and the lender begins the legal process of reclaiming the property. This is a critical stage where you still have time to act before foreclosure is finalized. If your lender has contacted you about missed payments, ignoring the situation will only make things worse. The sooner you take action, the more options you’ll have to protect your home, your credit, and your financial future

GET MORE INFORMATION

WHAT ARE YOUR OPTIONS?

The good news is that pre-foreclosure is not the end of the road. You still have several options available, including:

🔹 Loan Modification – Some lenders will work with you to adjust your mortgage terms, lower your monthly payments, or extend your loan period to make it more manageable.

🔹 Forbearance – If you’re facing temporary financial hardship, your lender may agree to pause or reduce your payments for a certain period of time.

🔹 Short Sale – If your home is worth less than what you owe, you may be able to negotiate a short sale, where the bank agrees to let you sell the property for less than the remaining mortgage balance.

🔹 Selling Your Home Before Foreclosure – If you still have equity in your home, you might be able to sell it for a fair price and walk away with cash instead of letting the bank take it. Many homeowners choose this route to avoid foreclosure’s long-term financial consequences.